Organon Is Telling You Exactly What It Is and the Exit Math for Women's Health Has Changed

The sequence of decisions Organon made between October 2025 and March 2026 changes the exit landscape for every early-stage company building in reproductive health and hormonal therapeutics

📕Special note: My book The Billion Dollar Blindspot is available for pre-order on Amazon. It’s currently #3 on Amazon hot new releases in our category. Will you help me make it to #1?

The most important acquirer in women’s health pharmaceuticals is subtly telling the market what it has become. Its not doing so through a press release but rather through a sequence of decisions made between October 2025 and March 2026 that, read together, paint a specific picture. Most investors in this space are reading them separately and that is the gap.

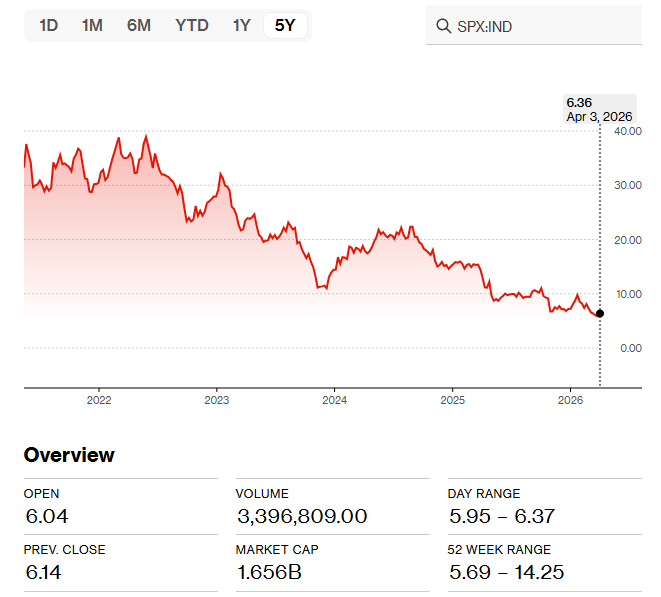

Organon, the MSD spin-out that holds Nexplanon, NuvaRing, and one of the largest women’s health commercial footprints in the world has spent the last five months selling assets, dropping R&D programs, licensing commercial-stage devices, running without a permanent CEO, and watching its share price sit roughly 63% below its three-year high. A non-binding acquisition approach from Sun Pharma surfaced in January, was publicly labelled speculative within days, and has since gone quiet.

What happened

Between October 2025 and March 2026, Organon:

lost its founding CEO to a Nexplanon sales irregularity investigation

reported full-year 2025 revenue of $6.2B against $8.64B in debt

cut its quarterly dividend to $0.02

discontinued its entire internal R&D pipeline for endometriosis and PCOS (both acquired via Forendo in 2021)

divested its JADA postpartum hemorrhage system for $465M

and licensed in MIUDELLA, the first new hormone-free copper IUD in the US in 40 years for $27.5M upfront.

In addition, guidance for FY 2026 is flat and the permanent CEO search is ongoing.

Why it matters

What Organon’s portfolio moves reveal is a deliberate strategic retreat: from originating science in women’s conditions toward distributing and commercialising proven products.

That is a rational response to $8.64B in debt and a governance crisis. It is also a structural shift in what Organon is and what it can offer the ecosystem that has been building toward it as an acquirer.

The endometriosis and PCOS pipeline drops are worth sitting with. These are two of the highest-unmet-need, highest-diagnostic-delay conditions in women’s health. Organon acquired rights to drug candidates in both, and has now walked away from both. At the same time, it licensed a commercial-stage contraceptive device.

That sequencing tells you something precise about what Organon is becoming. The more important question for anyone building or backing companies in this space is what that becoming means for where exits go from here.

Keep reading with a 7-day free trial

Subscribe to The Billion Dollar Blindspot to keep reading this post and get 7 days of free access to the full post archives.