When Women's Health Meets Institutional Capital

Why venture capital growth alone may not be enough for women's health to become an institutional investment category.

One of the privileges of a career in institutional investing is that you spend an extraordinary amount of time either watching a Bloomberg terminal or reading. Anything from reports, investment committee papers, fund manager due diligence questionnaires, academic journals, industry research and market commentary – all is fair game.

Over time, you stop reading individual reports in isolation. You begin reading them against each other, looking for contradictions, blind spots and patterns that only become visible when different pieces of information collide.

Two reports landed on my desk over the past few weeks.

The first was Silicon Valley Bank’s latest Innovation in Women’s Health report. The headlines were encouraging. Investment continues to flow into women’s health. New specialist funds are being launched. The ecosystem continues to mature.

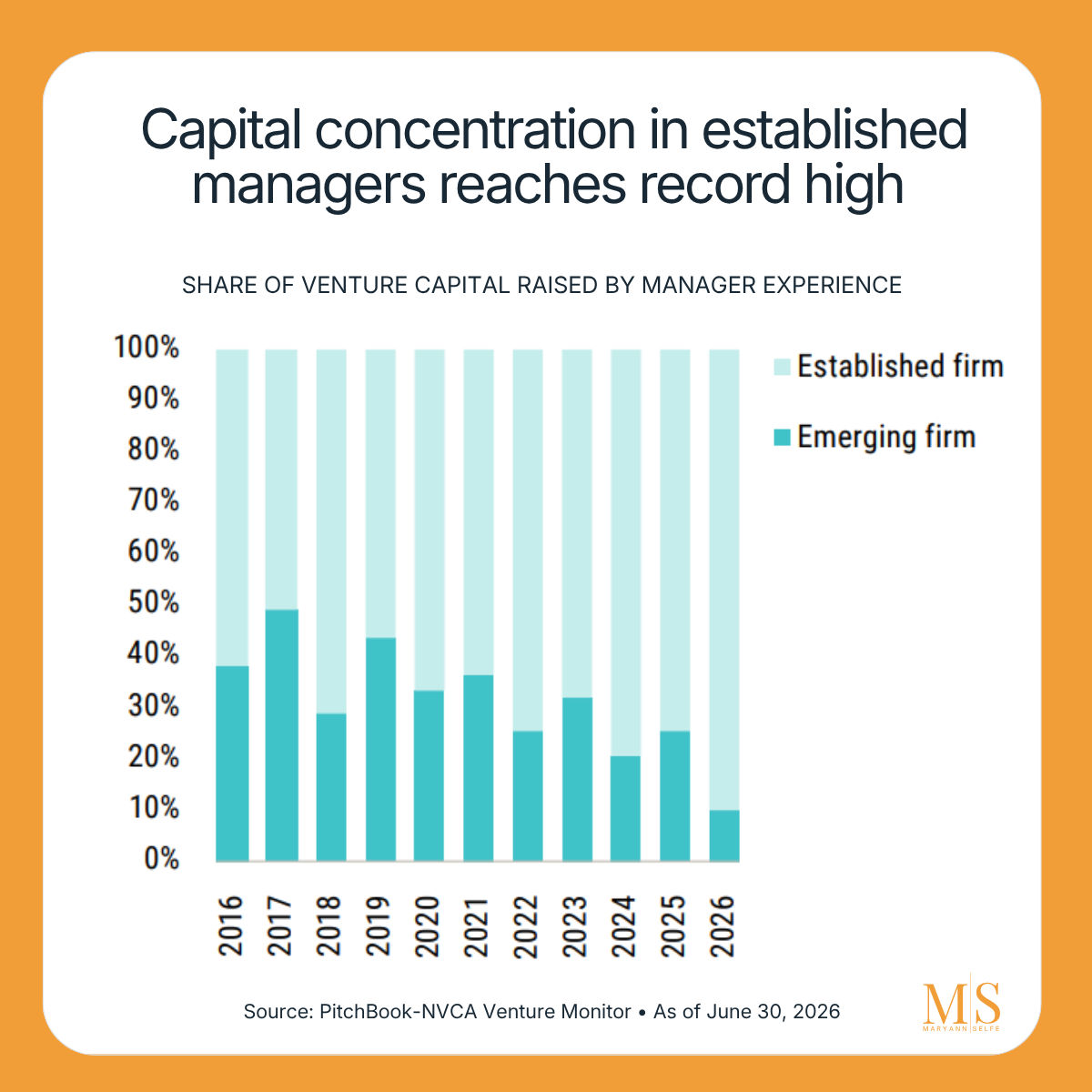

The second was PitchBook’s latest Venture Monitor, which showed that three established venture capital firms accounted for almost half (48.1%, to be precise) of all venture capital raised during the first half of 2026... and no, they were not women’s health-focused.

Individually, neither report surprised me.

Together, they made me question whether we’re looking at women’s health investment through the wrong lens.

The narrative surrounding women’s health has changed considerably over the past five years. For a long time, the conversation centred on neglect, lack of research and lack of funding.

Today, the narrative is more optimistic. Funding remains modest, but it is increasing. New companies are being founded. Dedicated investors are emerging. Large healthcare companies are beginning to size up potential acquisition targets.

While all of that is true, institutional investing teaches you to ask a slightly different question.

As allocators, we are trained to think in proportions rather than absolutes. Growth, by itself, tells us very little. Context tells everything. A market can double in size and still remain materially under-allocated.

Women’s health is no longer an emerging scientific curiosity. It sits at the intersection of some of the largest structural forces reshaping healthcare: demographic ageing, precision medicine, artificial intelligence, diagnostics, fertility, longevity and the growing recognition that sex-specific biology matters across almost every major disease area.

If those trends continue, and I believe they will, then women’s health is not simply another healthcare vertical. It becomes one of the defining investment themes of the coming decades.

Which brings me back to one of the starkest observations from the H1 2026 venture fundraising environment; Just three established venture capital firms accounted for almost half of all venture capital raised during the first six months of the year. In other words, fundraising remained highly concentrated among a small number of established managers.

Weekly capital intelligence on women’s health. Summer Special 20%

At this point, it’s worth explaining what institutional investors mean by an emerging manager.

Broadly speaking, these are independently owned investment firms still in the early stages of building their institutional business. Most are raising Fund I, II or III. Many are led by highly experienced investment professionals who have left established firms to build specialist platforms of their own.

This matters because the vast majority of specialist women’s health investment firms today are still at that stage. By institutional standards, many women’s health funds are emerging managers.

That, in itself, isn’t unusual. Every successful investment firm started as an emerging manager. Sequoia once raised Fund I. Andreessen Horowitz once raised Fund I. Every manager trusted with billions today had a first institutional investor.

Every institution now considered “blue chip” was once asking someone to believe before the track record existed.

But this is where the two reports began to collide in my mind.

Institutional capital overwhelmingly allocates to established managers. That is neither surprising nor wrong. It’s a feature of prudent fiduciary investing. Track record matters. Governance matters. Operational resilience matters. The ability to manage capital through multiple market cycles matters. These are exactly the characteristics institutional investors should evaluate.

But it also means that for a category like women’s health—which remains a relatively young investment category—many of the managers with the deepest domain expertise are still in the early stages of building institutional businesses and are therefore largely invisible to institutional capital.

That, I believe, is the conversation we are still not having.

Women’s health is often discussed as though the primary challenge is getting more venture capital into the sector. I wonder whether that is only half the story. Because venture capital is just one layer of the capital stack.

If women’s health is genuinely becoming one of healthcare’s defining investment themes (and I believe it is) then eventually the sector will need to attract not just venture capital, but long-term institutional capital; the long-term pools of capital capable of supporting the sector as it matures like pension funds, endowments, sovereign wealth funds and family offices.

But that requires us to zoom out.

The opportunity itself has never been clearer. Women account for roughly half of the world's population and make around 80% of healthcare purchasing decisions, yet continue to experience measurable gaps in research, diagnosis and treatment. At the same time, advances in precision medicine, artificial intelligence, diagnostics, genomics and longevity are transforming our understanding of sex-specific biology across almost every major disease area.

From an investment perspective, that combination represents one of the largest structural opportunities in modern healthcare. This is no longer simply a conversation about women’s health. It is a conversation about the future of healthcare.

And if that future is as significant as many of us believe it to be, then perhaps we should be asking a different question. Not simply, “Is capital increasing?” But, “Is capital increasing at a scale that reflects the opportunity?” Because those are two very different questions.

I’ve spent enough years sitting on investment committees to know that they lead to very different conversations. The first is about innovation. The second is about institutionalisation. One asks, “Is there an opportunity?” The other asks, “Can institutions responsibly access that opportunity?”

The distinction may appear subtle but I don’t think it is. In fact, I suspect it may become one of the defining questions for specialist healthcare investing over the next decade.

I don’t yet know the answer. But I increasingly believe we’re asking the wrong question.

So let me leave you with the one I haven’t been able to stop thinking about since those two reports landed on my desk.

If specialist women’s health investing is still largely being led by Fund I, II and III managers, and institutional capital overwhelmingly allocates to established firms, how do we create the conditions for women’s health to become an institutional investment category?

These ideas sit at the heart of my new book, The Billion Dollar Blindspot. The book explores how outdated assumptions shaped research, innovation, and investment in women’s health and why some of the most important opportunities in healthcare may emerge when those assumptions begin to break down.

I’m grateful that the book reached #1 New Release on Amazon in its category, a sign that more readers are beginning to engage with these ideas. Because this conversation is ultimately about much more than menopause, hormones, or even women’s health.

It is about what happens when we finally start looking at the world as it is, rather than as it used to be. If you’d like to explore these ideas more deeply, you can find The Billion Dollar Blind Spot on Amazon.

Key Takeaways

Institutional capital allocation vs. women’s health: While venture funding for women’s health is increasing, institutional investors should evaluate whether capital allocation is growing at a scale proportionate to the long-term opportunity, rather than focusing solely on year-over-year funding growth.

Emerging manager challenge: Most specialist women’s health investment firms are still emerging managers (typically raising Fund I, II or III). Institutional due diligence frameworks naturally favour established managers with long track records, governance maturity and operational scale, making many specialist managers difficult for institutions to access.

Capital concentration: PitchBook’s H1 2026 Venture Monitor found that three venture capital firms accounted for 48.1% of all venture capital raised, illustrating the continued concentration of fundraising among established managers and raising questions about how new specialist investment franchises are built.

Women’s health as a structural investment theme: Women’s health intersects with major long-term healthcare trends including demographic ageing, precision medicine, artificial intelligence, diagnostics, genomics and sex-specific medicine, making it a significant emerging investment theme rather than a niche healthcare category.

Core thesis: The next challenge for women’s health is not simply attracting more venture capital, but creating the conditions for it to become an institutional investment category by enabling long-term institutional investors to efficiently discover, evaluate and access specialist investment expertise.

Disclaimer & Disclosure

This content is for informational and educational purposes only. It does not constitute financial, investment, legal, or medical advice, or an offer to buy or sell any securities. Opinions expressed are those of the author and may not reflect the views of affiliated organisations. Readers should seek professional advice tailored to their individual circumstances before making investment decisions. Investing involves risk, including potential loss of principal. Past performance does not guarantee future results.